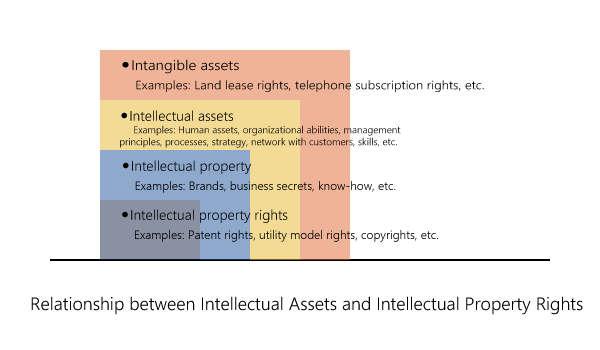

Relationship between Intellectual Assets and Intellectual Property Rights

Intellectual property rights are the right to be able to monopolize many acts.This gives economic incentive for their creation, because it allows people to profit from the intellectual property they create.

These are expected to stimulate innovation and contribute to the technological progress, depends on the protection granted to innovators.

The intellectual property right system is a system for protecting what is created by intellectual creation activities as the property of the creator. “Intellectual property” and “intellectual property right” are defined as follows in Article 2 of the Intellectual Property Basic Act.

この法律で「知的財産」とは、発明、考案、植物の新品種、意匠、著作物その他の人間の創造的活動により生み出されるもの(発見又は解明がされた自然の法則又は現象であって、産業上の利用可能性があるものを含む。)、商標、商号その他事業活動に用いられる商品又は役務を表示するもの及び営業秘密その他の事業活動に有用な技術上又は営業上の情報をいう。

この法律で「知的財産権」とは、特許権、実用新案権、育成者権、意匠権、著作権、商標権その他の知的財産に関して法令により定められた権利又は法律上保護される利益に係る権利をいう。

A patent is an exclusive right granted for an invention. Generally speaking, a patent provides the patent owner with the right to decide how - or whether - the invention can be used by others. In exchange for this right, the patent owner makes technical information about the invention publicly available in the published patent document.(WIPO)

A trademark is a sign capable of distinguishing the goods or services of one enterprise from those of other enterprises. Trademarks date back to ancient times when artisans used to put their signature or "mark" on their products.(WIPO)

A utility model is the right to exclusively and exclusively devise the invention relating to the shape, structure, and combination of articles, and a patent-like intellectual property right. it is generally cheaper to obtain and maintain, has a shorter term, shorter grant lag, and less stringent patentability requirements.

An industrial design constitutes the ornamental or aesthetic aspect of an article. A design may consist of three-dimensional features, such as the shape or surface of an article, or of two-dimensional features, such as patterns, lines or color.(WIPO)

Copyright is a legal term used to describe the rights that creators have over their literary and artistic works. Works covered by copyright range from books, music, paintings, sculpture and films, to computer programs, databases, advertisements, maps and technical drawings.(WIPO)

Integrated circuit layout, also known IC layout, IC mask layout, or mask design, is the representation of an integrated circuit in terms of planar geometric shapes which correspond to the patterns of metal, oxide, or semiconductor layers that make up the components of the integrated circuit.

Plant breeders' rights (PBR), also known as plant variety rights (PVR), are rights granted to the breeder of a new variety of plant that give the breeder exclusive control over the propagating material (including seed, cuttings, divisions, tissue culture) and harvested material (cut flowers, fruit, foliage).

Trade secrets are IP rights on confidential information which may be sold or licensed. The unauthorized acquisition, use or disclosure of such secret information in a manner contrary to honest commercial practices by others is regarded as an unfair practice and a violation of the trade secret protection.(WIPO)

Intellectual property rights require calculating the fair value in various aspects, but in M&A, Japan Generally Accepted Accounting Principles Business Combination requires that intangible assets be measured and calculating the fair value in order to allocate the acquisition cost to the acquired assets and liabilities at fair value and measure the excess as goodwill or negative goodwill. In PPA, not only legal rights but also assets that are received in a business combination through acquisition include "separable and transferable intangible assets", they are treated as identifiable assets, and the market value at the business combination date is used. Guidance on Accounting Standards No.10 Paragraphs 59 and 367 stipulate the following:

「分離して譲渡可能な無形資産」とは、受け入れた資産を譲渡する意思が取得企業にあるか否かにかかわらず、企業又は事業と独立して売買可能なものをいい、そのためには、当該無形資産の独立した価格を合理的に算定できなければならない。

分離して譲渡可能な無形資産であるか否かは、対象となる無形資産の実態に基づいて判断すべきであるが、例えば、ソフトウェア、顧客リスト、特許で保護されていない技術、データベース、研究開発活動の途中段階の成果(最終段階にあるものに限らない。)等についても分離して譲渡可能なものがある点に留意する。

As there is no comprehensive accounting standard for intangible assets in Japan, IFRS 3 (International Financial Reporting Standards) and IAS 38 (International Accounting Standard) are used as a practical reference. IFRS 3 IE18-44 shows examples of identifiable intangible assets as shown in the table below. In the table, C:Contractual is an intangible asset that satisfies contract and legal requirements, and N:Non-contratual is an intangible asset that satisfies separability requirements.

Marketing

-related

IFRS3

IE18-22

| C | Trademarks, trade names, service marks, collective marks and certification marks |

|---|---|

| C | Trade dress (unique colour, shape or package design) |

| C | Newspaper mastheads |

| C | Internet domain names |

| C | Non-competition agreements |

Customer

-related

IFRS3

IE23-31

| N | Customer lists |

|---|---|

| C | Order or production backlog |

| C | Customer contracts and related customer relationships |

| N | Non-contractual customer relationships |

Artistic

-related

IFRS3

IE32-33

| C | Plays, operas and ballets |

|---|---|

| C | Books, magazines, newspapers and other literary works |

| C | Musical works such as compositions, song lyrics and advertising jingles |

| C | Pictures and photographs |

| C | Video and audiovisual material, including motion pictures or films, music videos and television programmes |

Contract

-based

IFRS3

IE34-38

| C | Licensing, royalty and standstill agreements |

|---|---|

| C | Advertising, construction, management, service or supply contracts |

| C | Lease agreements (whether the acquiree is the lessee or the lessor) |

| C | Construction permits |

| C | Franchise agreements |

| C | Operating and broadcast rights |

| C | Servicing contracts, such as mortgage servicing contracts |

| C | Employment contracts |

| C | Use rights, such as drilling, water, air, timber cutting and route authorities |

Technology

-based

IFRS3

IE39-44

| C | Patented technology |

|---|---|

| C | Computer software and mask works |

| N | Unpatented technology |

| N | Databases, including title plants |

| C | Trade secrets, such as secret formulas, processes and recipes |

According to the Ministry of Economy, Trade and Industry, ”Intellectual assets” become the business core and other intellectual assets (human assets, organizational assets, relationship assets). They are also considering that the relationship between intellectual property rights, intellectual property, intellectual assets, and intangible assets can be organized as follows. The intangible assets signify all intangible business resources held by the

enterprise, which is not the same meaning as intangible fixed assets recorded in the

balance sheet.

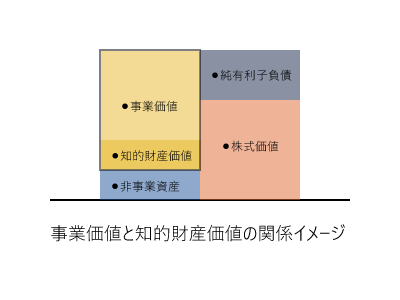

評価対象は、「知的財産」や「無形資産」に限らず、特に、資金調達局面やM&A局面などにおいて、「株式価値」、「事業価値」の評価も対応しております。知的財産価値と事業価値の関係性は以下イメージとなります。知的財産の寄与度が100%であれば、知的財産価値=事業価値となりますが、一般的に各企業のビジネスモデルによって大きく異なります。参考までに、企業の収益は、資本、組織、労働、技術の4つの要素(又は、技術開発、製品開発、製造、販売の4つの要素)の成果として、知的財産関連事業から得られる利益の25%を実施料とする考え方(ルールオブサム法:25%ルール)もあります。

Patent Valuation Advisory is a professional firm that specializes in evaluating intellectual property such as patent rights.